Speech – Current Assessment of Financial Stability

May 8, 2024 / Source: FRB

Governor Lisa D. Cook

Thank you, David. And thank you to the Brookings Institution for hosting me today. I am especially grateful to return to the place where, in my first job as an aspiring economist, I was a research assistant for Alice Rivlin over three decades ago.

Today, I would like to talk about the Board’s work in pursuit of financial stability, which is critical to the well-being of households, firms, and the broader economy.1 Following the financial crisis of 2007–09, a broad set of reforms were put in place to bolster financial stability. To ensure an ongoing focus on that area, the Board established its Committee on Financial Stability as a venue for Governors to discuss related developments and policy issues. I recently became the chair of this committee and will share with you my current views on financial stability and touch on a couple of emerging issues. Enhancing the public’s understanding of our work on financial stability is important for the transparency and accountability of our efforts. That is why we communicate our financial stability work prominently in our Financial Stability Report, which was most recently published last month and provides more detail on some of the developments I will review today.2

Financial Stability at the Federal Reserve

As the U.S. and global financial system continues to grow and evolve in complexity, the Fed’s work on financial stability only becomes more important. A stable and resilient financial system is essential for the Federal Reserve to achieve its dual mandate of maximum-employment and price-stability. Our financial stability work also informs our approach and priorities to the supervision and regulation of banking organizations, our coordination with domestic regulatory agencies, and our engagements with international bodies such as the Financial Stability Board.

Financial Stability Framework

When people think about financial stability, they most often recall periods affected by adverse shocks—that is, severe, unexpected events that cause widespread disruptions to the financial markets and, in turn, the broader economy. The challenge is that such events are hard to predict.

Therefore, the Fed’s financial stability framework focuses on understanding what makes the financial system vulnerable to a whole range of potential shocks and how those vulnerabilities might amplify the effects of those shocks, not on predicting specific adverse events.

Review of Vulnerabilities

Based on extensive research and experience, we routinely monitor four broad sets of vulnerabilities to the financial system that could amplify shocks: household and business leverage; the use of leverage by financial institutions; the degree of maturity and liquidity transformation in the financial system, or, in plain English, “funding risk”; and asset valuations and risk appetite.

Household and Firm Leverage

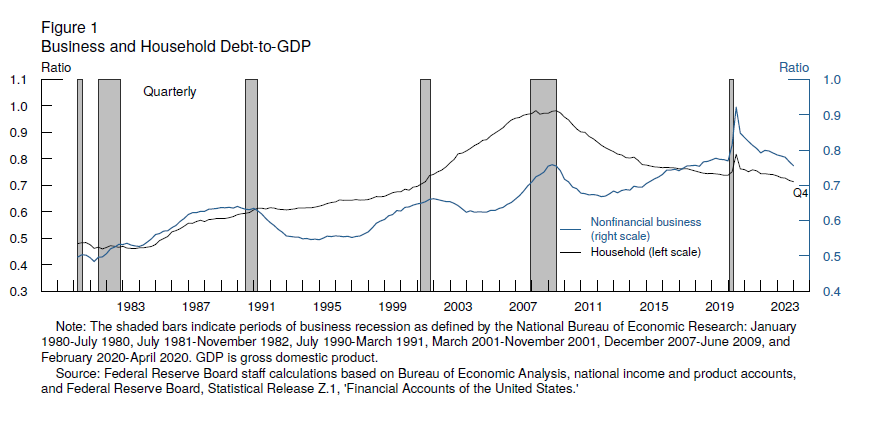

To lay out how I am currently thinking about each of these vulnerabilities, I will start with household and firm leverage. A simple measure of whether households or firms are borrowing too much is to compare their debt to the level of GDP, as shown in figure 1. Based on this measure, household borrowing is lower than it has been in many years. Our analysis then dives deeper, including detailed assessments of mortgage borrowing and consumer credit, and this deeper assessment supports the view of a resilient household sector. Nonetheless, we also are attuned to possible changes in this assessment. For example, I am watching closely the rising delinquency rates on auto loans and credit card debt—both of which partially reflect a normalization from recent lows—because they imply increasing household borrower stress, especially among some lower- and moderate-income households.

{kind=link}

From the figure, you can also see that, looking through the unusual pandemic period, business debt relative to GDP remains above historical norms. Despite this, most firms still have ample earnings to cover their scheduled interest and principal payments. This solid position reflects resilient earnings and the fact that firms with access to bond markets locked in long-term funding during the low interest rate environment of 2020 and 2021. As a result, most firms also appear, in broad terms, resilient to potential adverse shocks.

Financial Leverage and Funding Risk

Let me turn now to the leverage and funding risk in the financial sector.

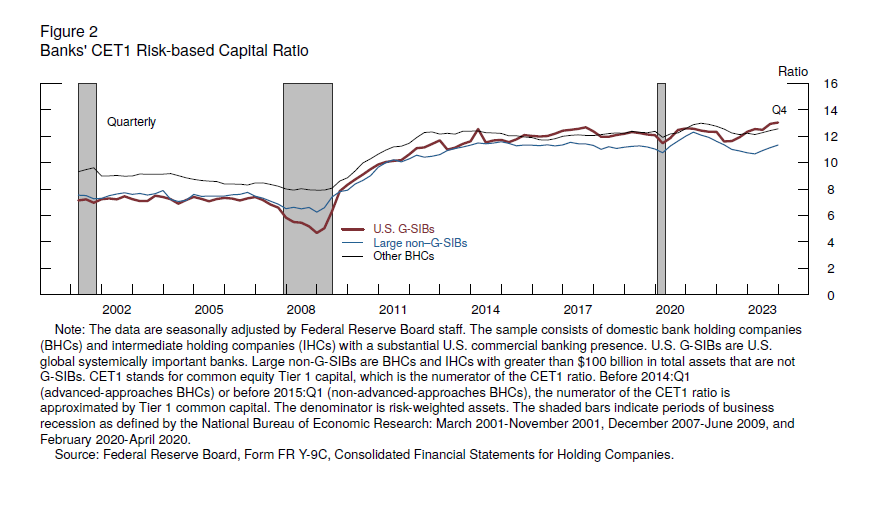

In assessing these vulnerabilities, we tend to place a lot of weight on the capital adequacy and liquidity of the largest and most interconnected financial firms. Currently, these firms appear well positioned to absorb a shock. For instance, figure 2 shows the ratio of common equity tier 1 capital to risk-weighted assets—a standard regulatory capital measure—for three groups of banks. This ratio has been increasing for all types of banks lately and, for the largest banks, stands at multidecade highs. The largest banks also have strong funding profiles, owing in part to the strength of the regulatory regime for these banks.

{kind=link}

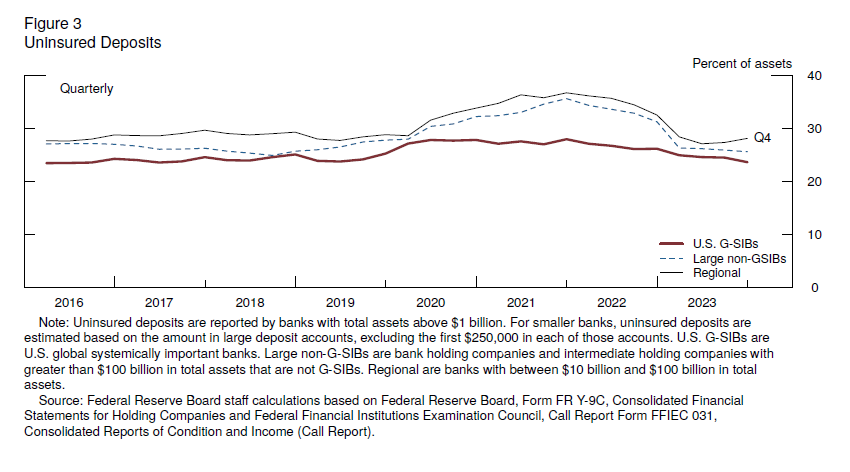

Despite the overall resilience of the banking sector, some regional banks experienced large deposit outflows amid the failures of three banks last spring. Conditions have improved considerably since then: Bank profitability remains solid, and deposit flows have stabilized. In addition, as shown in figure 3, most institutions have lowered their reliance on uninsured deposits since the beginning of 2023. We remain attuned to vulnerabilities in this sector. Supervisors are working closely with the set of banks that have experienced outsized fair-value losses from higher interest rates and with banks that have high concentrations of commercial real estate loans.

{kind=link}

We have varying levels of visibility into the leverage and funding vulnerabilities of other financial intermediaries. While there are some areas of apparent vulnerability, there is also evidence of resilience. Hedge fund leverage is hard to measure, but available data suggest that these funds’ leverage is near the high end of its range. Large insurers are well capitalized, but they have been increasing their use of liabilities subject to rollover risk at the same time as they have raised the portion of their assets invested in riskier corporate debt instruments. Money funds have inherent funding vulnerabilities that regulators have been taking steps to address. Reforms adopted by the SEC and coming into force this year will improve funds’ liquidity positions and address the structural first-mover advantages among money fund investors that contributed to some of the runs we have seen in this sector over the years.

Asset Valuations

Let me turn now to asset valuations. I think it is helpful to consider this potential vulnerability in the context of how a sharp change in valuations could interact with the vulnerabilities I have already discussed. I will start with the classic concern for all of us who lived through the Great Recession: A large decline in asset prices against the backdrop of a weak economy. For example, house prices are high relative to historical benchmarks, likely owing partly to a limited supply of homes for sale. What might the implications be if house prices were to weaken at some future date?

The house-price growth we have seen over the past few years has not been accompanied by increased lending or weaker credit standards, as was the case in the early 2000s. The household sector also is much more resilient than in 2006. One way to see this is to run the distribution of risk characteristics we see in the household sector through a constant set of income and house-price shocks.3 The stronger underwriting standards that have prevailed since the post-crisis reforms went into place and stronger household balance sheets mean that post-stress delinquency rates should be lower the next time we experience a housing shock. Finally, the financial system is in substantially stronger shape to resist any losses that do occur: The largest banks are subject to stress tests that require them to be able to continue to function through a severe recession, and important structural improvements have been implemented among nonbank entities.

Commercial Real Estate

Now I will turn to commercial real estate, or “CRE,” where the shocks created by the COVID-19 pandemic continue to reverberate.

CRE is a broad asset class, encompassing multifamily housing, hospitality, retail, warehouses, office buildings, and many other business properties. Accounting for this heterogeneity is important in assessing the risks associated with CRE. Properties have been differentially impacted by changes in the way many people live, shop, and work. For instance, occupancy rates of suburban medical offices are very different from those of downtown corporate headquarters. Looking at broader trends, values of office buildings have been most affected by lifestyle changes, and values of multifamily properties have also dropped over the past year. These trends present challenges for property owners and lenders, who will need to manage those risks and make appropriate adjustments as the outstanding loans come due.

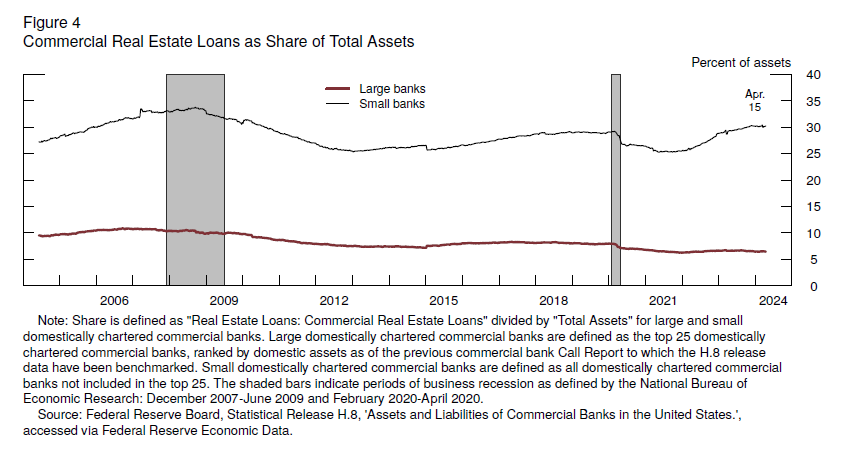

As of the fourth quarter of last year, banks accounted for a bit more than half of the $6 trillion in outstanding debt backed by CRE. Figure 4 shows that much of that exposure is in smaller regional and community banks. On average, CRE loans make up only about 5 percent of total assets at large banks but around 30 percent of assets at smaller banks. Those high concentrations have caused us to step up our supervisory work with community and regional banks that have significant CRE concentrations and to augment our regulatory data for this sector. For instance, data available from SEC Form 10-Q filings suggest that office exposures account for a small share of most regional banks’ CRE loans.4 All told, I view CRE risks currently as sizable but manageable, and I will be paying close attention to the sector in the short and medium run.

{kind=link}

Private Credit

Risks related to CRE are well known to investors and supervisors alike. Another big part of our job is to look for emerging vulnerabilities, and one that has garnered my attention is private debt. Private credit generally refers to direct loans made to businesses, mostly middle-market firms, by nonbank entities such as private debt funds and business development companies. In the U.S., private credit funds’ assets under management have grown rapidly in recent years. They were estimated to stand at $1.1 trillion as of September 2023, comparable in size to both the high-yield bond and institutional leveraged-loan markets.

History teaches us that rapidly growing lending often involves weak underwriting or excessive risk appetite. The growth in private credit is likely attributable to a confluence of factors. After the financial crisis of 2007–09, private equity investments and leveraged buyouts grew quickly, and demand for credit from middle-market and private equity-sponsored firms grew along with them. Some borrowers appear to prefer private credit deals to bank lending because of easier deal execution and greater contractual flexibility, particularly during the ups and downs of the economic cycle. In addition, the growth of private credit coincided with a period in which stronger bank regulation and supervision were put in place, suggesting that those actions to make banks safer played a role.

Overall, I think that the growth of private credit likely has not materially adversely affected the financial system’s resilience. Private credit funds appear well positioned to hold the riskiest parts of corporate lending. These intermediaries generally use little leverage and are organized as closed-end funds, which means that investors cannot withdraw the funding supporting the investments. Nonetheless, private credit funds also have growing interconnections with traditional financial intermediaries, including banks. Banks are increasingly originating their own private credit deals—such as through business development companies that are operated or minority-owned by the banks themselves. As a result, I will be monitoring the contribution of private credit to the overall leverage of the business sector and the evolving interconnectedness between private credit and the rest of the financial system.

Cyber Risks and Financial Stability

I will conclude with a few thoughts on cyber risk. I should emphasize at the outset that the Federal Reserve’s role in managing cyber vulnerabilities is focused primarily on ensuring the institutions we supervise effectively manage the cyber risks they face, including from key technology service providers to those institutions, and safeguarding the resilience of the services provided by the Federal Reserve and the financial system more broadly in the event of a successful attack. We also work with our partners across the government, including the U.S. Department of the Treasury, and with the private sector to understand and address cyber risks.

Over the past few years, we have seen an accelerating tempo of cyberattacks from a mix of groups associated with criminal enterprises and hostile governments. While the news sometimes seems dominated by ransomware attacks, we also continue to observe other types of attacks, such as those that seek to uncover information from governments and firms or to carry out or plant the seeds for destructive attacks on information systems that could severely disrupt operations.

In response to these risks, we are examining cyber incidents carefully to make sure we have a fuller understanding of how attacks can affect the financial system, including through banks, nonbank financial firms, digital service providers, and critical infrastructure. In this work, we focus heavily on the operational resilience of the institutions we supervise, the service providers used by such institutions, and the financial services provided by the Federal Reserve. We have also begun to incorporate analysis of timely data on firm-level cyber vulnerabilities and interconnections across firms and with service providers to monitor cyber vulnerabilities at the system level.

As we contemplate future incidents, my view is that financial resilience can also play a crucial role in mitigating the adverse effects of cyberattacks. Cyberattacks erode the confidence that investors and institutions have in each other and in the financial sector. While strong capital and liquidity positions will not, by themselves, prevent an intrusion, they leave the affected institution in a better position to rejoin the system once the attack is resolved and, most importantly, promote confidence among its counterparties. Moreover, the effects of chaotic markets may impact other institutions that suddenly face losses whose magnitudes might be hard to judge. Well capitalized, highly liquid, and well managed institutions will be best positioned to manage such difficult circumstances.

Conclusion

Let me conclude by summarizing how we approach the set of issues I have discussed—including systemwide monitoring, CRE and private credit developments, and cyber risks—in our financial stability work. We cannot know the next shock that will test the resilience of the financial system. That is why we focus on the resilience of the financial sector in our regulatory and supervisory work concerning banking organizations and in our engagement with other regulators. We also continuously monitor the financial system and regularly report our assessments in the Financial Stability Report. Such public communication contributes to the transparency and accountability of our efforts. I hope it also stimulates a public discussion of vulnerabilities to financial stability, as my colleagues and I value the range of views on these issues held across researchers, financial market participants, and the broader public. For this reason, I look forward to our discussion.

Again, thank you to the Hutchins Center and the Brookings Institution for hosting me today.

1. The views expressed here are my own and are not necessarily those of my colleagues on the Federal Reserve Board or the Federal Open Market Committee. Return to text

2. See Board of Governors of the Federal Reserve System (2024), Financial Stability Report (PDF) (Washington: Board of Governors, April). Return to text

3. An example of this kind of analysis can be found in Neil Bhutta, Jesse Bricker, Lisa J. Dettling, Jimmy Kelliher, and Steven M. Laufer (2019), “Stress Testing Household Debt,” Finance and Economics Discussion Series 2019-008 (Washington: Board of Governors of the Federal Reserve System, February). Return to text

4. Regional banks in this context are banks that have between $10 billion and $100 billion of total assets. This information reflects staff calculations based on data collected from a representative sample of individual banking organizations’ SEC Form 10-Q filings for the third quarter of 2023. Return to text