WASHINGTON — The Federal Deposit Insurance Corporation (FDIC) Board of Directors today adopted a final rule to amend part 328 of its regulations to modernize the rules governing use of the official FDIC signs and advertising statements, and to clarify the FDIC’s regulations regarding false advertising, misrepresentations of deposit insurance coverage, and misuse of the FDIC’s name or logo.

“The banking industry and practices have substantially changed since the FDIC official sign and advertising rules were last significantly updated in 2006.” said Chairman Gruenberg. “The revisions extend the certainty and confidence that the FDIC official sign provides at bank branch teller windows to the digital channels through which depositors are increasingly handling their banking needs.”

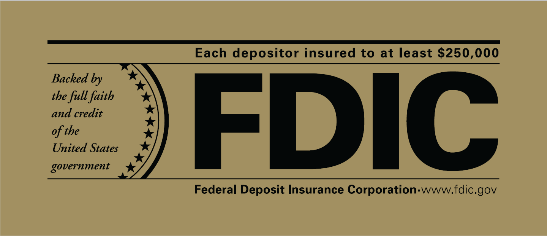

Since the 1930s, the black and gold FDIC official sign (shown below) displayed at bank branch teller windows has given bank customers confidence that their deposited funds are safe. Depositors and consumers today have a variety of options for where they can deposit their money and how they can access banking products and services. The revisions in the final rule extend the certainty and confidence associated with the FDIC official sign to digital channels, such as bank websites and mobile applications, through which depositors are increasingly handling their banking needs.

FDIC Official Physical Sign:

The final rule establishes a new black and navy blue FDIC official digital sign (shown below). Beginning in 2025, banks will be required to display the FDIC official digital sign near the name of the bank on all bank websites and mobile applications. Banks also will be required to display the FDIC official digital sign on certain automated teller machines.

FDIC Official Digital Sign:

In addition, the final rule modernizes requirements for display of the FDIC official sign in bank branches and other physical premises to account for evolving designs of bank branches and other physical bank locations where customers make deposits.

The final rule also requires the use of signs to differentiate insured deposits from non–deposit products across banking channels and to indicate that certain financial products “are not insured by the FDIC, are not deposits, and may lose value.”

The final rule clarifies the FDIC’s regulations regarding misrepresentations of deposit insurance coverage by addressing specific scenarios where a person, including a non–bank entity, provides information to consumers that may be misleading, confuse consumers as to whether they are doing business with a bank, and whether their funds are protected by deposit insurance. For example, the final rule clarifies that FDIC–associated terms or images may not be used in marketing and advertising materials to inaccurately imply or represent that any uninsured financial product or non–bank entity is insured or guaranteed by the FDIC.

The final rule complements the FDIC’s recently launched “Know your Risk. Protect your Money.” public awareness campaign, which is aimed at helping consumers better understand deposit insurance and how it protects their money.

The amendments made by the final rule will take effect on April 1, 2024, with an extended compliance date of January 1, 2025.

FDIC: PR-110-2023

https://www.fdic.gov/news/press-releases/2023/pr23110.html

- April 1, 2024

- Time: All Day

Other events in Effective Date

- January 8, 2018: Final Rule: CRA Amendments

- January 8, 2018: Effective Date: Payday, Vehicle Title, and Certain High-Cost Installment Loans

- May 31, 2018: Effective Date: Real Estate Appraisals

- January 27, 2018: SAR Update and Revision

- January 8, 2018: Effective Date: Revisions to Call Report

- September 21, 2018: Effective Date: Small Bank Holding Company and Savings and Loan Holding Company Policy Statement

- June 18, 2018: Transition to Two-Business-Day Standard Securities Settlement Cycle

- September 21, 2018: Final Rule: 2018 HMDA Final Rule on Partial Exemptions to the EGRRCPA

- August 28, 2018: Final Rule: Amendment to Regulation P

- September 21, 2018: Effective Date: Regulation V Summaries of Rights Under FCRA

- June 18, 2018: Effective Date: Securities Transaction Settlement Cycle

- September 14, 2018: Effective Date: Truth in Lending (Regulation Z) Annual Threshold Adjustments

- October 8, 2018: Effective Date: Reg. CC Availability of Funds and Collection of Checks

- November 27, 2018: Effective Date: Final Amendments to Regulation J

- December 3, 2018: Effective Date: Appraisals for Higher-Priced Mortgage Loans Exemption Threshold

- December 3, 2018: Effective Date: Consumer Leasing (Regulation M)

- February 10, 2019: Effective Date: Expanded Examination Cycle

- April 9, 2019: Effective Date: Implementation and Transition of the Current Expected Credit Losses Methodology

- April 9, 2019: Effective Date: Disclosure of Financial and Other Information by FDIC-Insured State Nonmember Banks

- December 3, 2018: Effective Date: EGRRCPA, SEC. 302. PROTECTING VETERANS’ CREDIT

- April 9, 2019: Effective Date: Private Flood Insurance Final Rule

- June 5, 2019: Effective Date: Final rule to implement a new section of the Home Owners’ Loan Act

- June 5, 2019: Effective Date: Liquidity Coverage Ratio Rule

- June 28, 2019: Effective Date: Reduced Reporting for Covered Depository Institutions

- August 6, 2019: Effective Date: Revisions to Prohibitions and Restrictions on Proprietary Trading and Certain Interests In, and Relationships With, Hedge Funds and Private Equity Funds

- August 6, 2019: Effective Date: Joint Ownership Deposit Accounts

- July 15, 2019: Effective Date: Availability of Funds and Collection of Checks (Regulation CC)

- October 8, 2018: Effective Date: NACHA Faster Funds Availability Rule

- July 15, 2019: Effective Date: Regulatory Capital Simplification Final Rule

- November 8, 2019: Effective Date: Increased Threshold for Residential Appraisal Exemptions

- August 30, 2019: Effective Date: FHFA Issues Final Rule Regarding Credit Score Models

- November 22, 2019: Effective Date: USDA Establishment of a Domestic Hemp Production Program

- December 3, 2018: Effective Date: EGRRCPA, SEC. 106. ELIMINATING BARRIERS TO JOBS FOR LOAN ORIGINATORS

- October 8, 2019: Effective Date: Amendments to the Stress Testing Rule for National Banks and Federal Savings Associations

- November 22, 2019: Effective Date: Screening and Training Requirements for Mortgage Loan Originators with Temporary Authority

- January 21, 2020: Effective Date: Temporary Reg. O relief for certain extensions of credit to fund complex-controlled portfolio companies

- January 6, 2020: Effective Date: Truth in Lending Act (Regulation Z) Adjustment To Asset-Size Exemption Threshold

- August 19, 2019: Effective Date: CFPB Issues Final Rule Adjusting the Annual Thresholds under Reg Z for 2020

- October 8, 2019: Effective Date: Department of Labor Final Rule to Update Overtime Compensation Regulations

- January 6, 2020: Effective Date: Home Mortgage Disclosure (Regulation C) Adjustment to Asset-Size Exemption Threshold

- January 21, 2020: Effective Date: OCC Issues Notice of Civil Money Penalties Adjustment

- February 7, 2020: Effective Date: Agencies Release Final Rule to Increase Asset-Size Thresholds for CRA

- January 31, 2020: Effective Date: Real Estate Appraisals Final Rule

- February 7, 2020: Effective Date: FRB Asset Threshold Adjustment in Regulation I

- October 8, 2018: Effective Date: NACHA Increase in the Per-Transaction Dollar Limit

- April 24, 2020: Applicability Date: Regulation D Reserve Requirements of Depository Institutions

- March 31, 2020: Effective Date: Interim Final Rule and Request for Comment to Revise CECL Implementation

- July 15, 2019: Effective Date: Regulatory Capital Simplification Final Rule (April 1, 2020)

- April 1, 2020: Effective Date: Regulatory Capital Treatment for HVCRE Exposures

- June 26, 2020: Applicability Date: FDIC Final Rule Regarding Mitigating the Deposit Insurance Assessment for Participating in PPP, PPPLF, and MMMFLF

- April 14, 2020: Effective Date: Federal Reserve Issues Interim Final Rule to Allow Revise Total Leverage Coverage

- April 15, 2020: Effective Date: PPP Interim Final Rule #1

- April 15, 2020: Effective Date: PPP Interim Final Rule #2

- April 17, 2020: Effective Date: Interim Final Rule and Request for Comment to Suspend Certain Appraisal and Evaluation Requirements

- April 22, 2020: FRB Interim Final Rule Regarding Reg O and PPP Loans

- April 23, 2020: Effective Date: Agencies Issue Interim Final Rule and Request for Comment to Regarding a Graduated Transition to Community Bank Leverage Ratio Framework

- April 23, 2020: Effective Date: Interim Final Rule and Request for Comment to Revise Community Bank Leverage Ratio Framework

- April 28, 2020: Effective Date: Regulation D Amendments

- April 27, 2020: Effective Date: CFPB Interpretive Rule Regarding Stimulus Checks and the Regulation E Compulsory Use Prohibition

- May 4, 2020: Effective Date: CFPB Interpretative Rule Regarding TRID and Right of Rescission

- May 6, 2020: Effective Date: Modification to the LCR Rule

- May 20, 2020: Effective Date: DOL Section 7(i) Exemption Final Rule

- May 12, 2020: Interim Final Rule: Deadline for Submission of the Initial SBA Form 1502

- June 5, 2020: Effective Date: PPP Flexibility Act

- April 23, 2020: Comment Period: Agencies Issue Interim Final Rule and Request for Comment to Regarding a Graduated Transition to Community Bank Leverage Ratio Framework

- June 26, 2020: Effective Date: Determining “Underserved” Areas Using HMDA Data

- June 26, 2020: Effective Date: FDIC Final Rule Regarding Mitigating the Deposit Insurance Assessment for Participating in PPP, PPPLF, and MMMFLF

- June 30, 2020: Last day for lenders to obtain an SBA loan number for PPP loans!

- July 15, 2019: Effective Date: Availability of Funds and Collection of Checks (Regulation CC) (July 1)

- June 30, 2020: Effective Date: Treatment of Certain COVID-19 Related Loss Mitigation Options Under RESPA

- May 12, 2020: Effective Date: CFPB Final Rule Regarding HMDA Thresholds

- July 6, 2020: Effective Date: S.4116 Extending the PPP to August 8, 2020

- July 1, 2020: Extended: IRA Contribution Deadline for 2019

- July 16, 2020: Effective Date: Reg. O Interim Final Rule to extend PPP exception to August 8, 2020

- July 20, 2020: Effective Date: Reg. E Remittance Transfer Rule 2020 Amendments

- August 13, 2020: Effective Date: OCC Interim Final Rule Regarding Collective Investment Funds

- June 30, 2020: Comment Period: Treatment of Certain COVID-19 Related Loss Mitigation Options Under RESPA

- July 23, 2020: Effective Date: Federal Interest Rate Authority

- June 25, 2020: Effective Date: FHFA amendments to FHLB Housing Goals regulation

- September 3, 2020: Effective Date: Small Business Administration Issues Interim Final Rule Regarding Paycheck Protection Program Nonpayroll Costs

- September 3, 2020: Effective Date: Small Business Administration Issues Interim Final Rule Regarding Paycheck Protection Program Loan Appeals

- September 18, 2020: Effective Date: Truth in Lending (Regulation Z) Annual Threshold Adjustments 2021

- August 1, 2020: Effective Date: Final Rule to Amend Volcker Rule

- September 4, 2020: Effective Date: Regulatory Capital Rule: Temporary Changes to and Transition for the Community Bank Leverage Ratio Framework

- July 23, 2020: Effective Date: Payday, Vehicle Title, and Certain High-Cost Installment Loans

- November 17, 2020: Effective Date: FDIC Issues Final Rule

- November 17, 2020: Effective Date: The OCC, Board, and FDIC (collectively, the agencies) issues Final Fule

- July 20, 2020: Effective Date: Truth in Lending (Reg. Z) Annual Threshold Adjustments

- September 4, 2020: Effective Date: Federal Reserve Issues Interim Final Rule to Allow Banks to Revise the Retained Income Defintion

- February 23, 2021: Effective Date: Final Margin Rule

- February 9, 2021: Effective Date: Qualified Mortgage Definition Under the Truth in Lending Act (Regulation Z): Seasoned QM Loan Definition

- February 9, 2021: Effective Date: Qualified Mortgage Definition Under the Truth in Lending Act (Regulation Z): General QM Loan Definition

- February 22, 2021: Effective Date: FDIC Issues Final Rules to Rescind and Remove Transferred OTS Regulations.

- February 22, 2021: Effective Date: Removal of Transferred OTS Regulations Regarding Certain Subordinate Organizations of State Savings Associations

- February 22, 2021: Effective Date: Removal of Transferred Office of Thrift Supervision (OTS) Regulations Regarding Nondiscrimination Requirements

- February 22, 2021: Effective Date: Removal of Transferred OTS Regulations Regarding Prompt Corrective Action Directives and Conforming Amendments to Other Regulations

- February 18, 2021: Effective Date: FRB Finalizes Regulation D Reserve Requirements

- February 23, 2021: Effective Date: Position Limits for Derivatives

- February 22, 2021: Effective Date: Disclosure of Payments by Resource Extraction Issuers

- October 8, 2018: Effective Date: NACHA New Same Day ACH Processing Window with Expanded Hours

- January 6, 2020: Effective Date: FRB Approves Changes to Federal Reserve Banks’ Payment Services to Facilitate Same Day ACH Processing at a Later Date

- February 9, 2021: Effective Date: Fair Access to Financial Services

- February 9, 2021: Effective Date: Unsafe and Unsound Banking Practices: Brokered Deposits and Interest Rate Restrictions

- February 9, 2021: Effective Date: Activities and Operations of National Banks and Federal Savings Associations

- February 9, 2021: Effective Date: Regulatory Capital Treatment for Investments in Certain Unsecured Debt Instruments of Global Systemically Important U.S. Bank Holding Companies, Certain Intermediate Holding Companies,

- February 23, 2021: Effective Date: Exemption from Definition of “Clearing Agency” for Certain Activities of Security-Based Swap Dealers and Security-Based Swap Execution Facilities

- February 18, 2021: Effective Date: Final Rule to Tailor Requirements in Capital Plan Rule

- May 26, 2021: Effective Date: Consolidated Reports of Condition and Income Changes June 30, 2021

- November 3, 2020: Effective Date: Final Rule on Net Stable Funding Ratio

- May 26, 2021: Effective Date: Consolidated Reports of Condition and Income Changes September 30, 2021

- November 4, 2021: Effective Date: Joint Statement on Managing the LIBOR Transition

- November 8, 2021: Effective Date: OSHA Emergency Temporary Standard

- February 18, 2021: Effective Date: Final Rule to Revise Regulation F

- May 12, 2020: Effective Date: CFPB Final Rule Regarding HMDA Thresholds

- November 8, 2021: Effective Date: Truth in Lending (Regulation Z) Annual Threshold Adjustments (Credit Cards, HOEPA, and Qualified Mortgages)

- March 24, 2022: Effective Date: OFAC Final Rule on Chinese Military-Industrial Complex Sanctions

- March 23, 2022: Effective Date: Interagency Statement on Special Purpose Credit Programs Under the Equal Credit Opportunity Act and Regulation B

- March 23, 2022: Mandatory Compliance: Russian Harmful Foreign Activities Sanctions Regulations

- March 23, 2022: Mandatory Compliance: Servicer Responsibilities in Public Service Loan Forgiveness Communications

- November 22, 2021: Effective Date: Computer-Security Incident Notification Requirements

- March 24, 2022: Effective Date: Computer-Security Incident Notification Requirements for Banking Organizations and Their Bank Service Providers

- March 23, 2022: Effective Date: FOMC formally adopts comprehensive new rules for investment and trading activity

- March 24, 2022: Effective Date: NACHA Rule on Micro-Entries

- December 13, 2022: Effective Date: CFPB- Fair Credit Reporting Act Disclosures

- December 13, 2022: Effective Date: FDIC- Assessments, Revised Deposit Insurance Assessment Rates

- January 30, 2023: Effective Date: Community Reinvestment Act: Revision of Small and Intermediate Small Bank and Savings Association Asset Thresholds

- January 30, 2023: Effective Date: Home Mortgage Disclosure (Regulation C) Adjustment to Asset-Size Exemption Threshold

- January 30, 2023: Effective Date: Truth in Lending Act (Regulation Z) Adjustment to Asset-Size Exemption Threshold

- January 30, 2023: Effective Date: Truth in Lending (Regulation Z) Annual Threshold Adjustments (Credit Cards, HOEPA, and Qualified Mortgages)

- January 30, 2023: Effective Date: Community Reinvestment Act Regulations Asset-Size Thresholds

- February 17, 2023: Effective Date: H.R. 2617

- February 17, 2023: Effective Date: Fair Credit Reporting Act Disclosures

- February 17, 2023: Effective Date: Supervisory Guidance on Multiple Re-Presentment NSF Fees

- February 17, 2023: Effective Date: Truth in Lending (Regulation Z) Amendment

- February 17, 2023: Effective Date: Consumer Leasing (Regulation M) Amendment

- December 13, 2022: Effective Date: FRB- Reserve Requirements of Depository Institutions

- February 17, 2023: Effective Date: Joint Statement on Crypto-Asset Risks to Banking Organizations

- February 17, 2023: Effective Date: Reserve Requirements of Depository Institutions

- February 17, 2023: Effective Date: Inflation Adjustment of Civil Monetary Penalties

- February 17, 2023: Effective Date: Inflation Adjustment of Civil Monetary Penalties

- February 17, 2023: Effective Date: Improvements to the Federal Reserve Policy on Payment System Risk

- February 22, 2023: Effective Date: Policy Statement on Section 9(13) of the Federal Reserve Act

- February 22, 2023: Effective Date: Regulation D rate of interest paid on balances (“IORB”) maintained at Federal Reserve Banks by or on behalf of eligible institutions

- February 22, 2023: Effective Date: Regulation A increase in the rate for primary credit at each Federal Reserve Bank

- February 22, 2023: Effective Date: Real Estate Settlement Procedures Act (Regulation X); Digital Mortgage Comparison-Shopping Platforms and Related Payments to Operators

- March 10, 2023: Effective Date: Electronic-Filing Requirements for Specified Returns and Other Documents

- March 10, 2023: Effective Date: Joint Statement on Liquidity Risks to Banking Organizations Resulting from Crypto-Asset Market Vulnerabilities

- January 30, 2023: Effective Date: Prior Approval for Enterprise Products

- February 17, 2023: Effective Date: Regulation Implementing the Adjustable Interest Rate (LIBOR) Act

- March 24, 2023: Effective Date: Supervisory Highlights Junk Fees Special Edition

- March 24, 2023: Effective Date: Fair Hiring in Banking Act Amends Section 19 of the Federal Deposit Insurance Act

- March 24, 2022: Effective Date: NACHA Rule on Micro-Entries Phase 2

- April 7, 2023: Effective Date: Regulation D: Reserve Requirements of Depository Institutions

- April 7, 2023: Effective Date: Regulation A: Extensions of Credit by Federal Reserve Banks

- March 10, 2023: Effective Date: Adjustable Rate Mortgages: Transitioning From LIBOR to Alternate Indices

- April 7, 2023: Effective Date: Agency Contact Information

- May 12, 2023: Effective Date: Joint Statement on Completing the LIBOR Transition

- May 12, 2023: Effective Date: Overdraft Protection Programs: Risk Management Practices

- May 12, 2023: Effective Date: Interagency Policy Statement on Allowances for Credit Losses

- May 12, 2023: Effective Date: Securities Transaction Settlement Cycle

- May 12, 2023: Effective Date: Corrections in the Iranian Transactions and Sanctions Regulations and Western Balkans Stabilization Regulations

- March 10, 2023: Effective Date: Prior Approval for Enterprise Products

- April 7, 2023: Effective Date: Reinstatement of HUD’s Discriminatory Effects Standard

- May 12, 2023: Effective Date: Fair Debt Collection Practices Act (Regulation F); Time-Barred Debt

- May 12, 2023: Effective Date: Supervisory Guidance on Charging Overdraft Fees for Authorize Positive, Settle Negative Transactions

- June 23, 2023: Effective Date: Shortening the Securities Transaction Settlement Cycle

- March 24, 2023: Effective Date: Increased Forty-Year Term for Loan Modifications

- June 2, 2023: Effective Date: Consumer Financial Protection Circular 2023-02

- April 28, 2023: Effective Date: Affiliation and Lending Criteria for the SBA Business Loan Programs

- June 2, 2023: Effective Date: Regulation D: Reserve Requirements of Depository Institutions

- June 2, 2023: Effective Date: Regulation A: Extensions of Credit by Federal Reserve Banks

- April 28, 2023: Effective Date: Small Business Lending Company (SBLC) Moratorium Rescission and Removal of the Requirement for a Loan Authorization

- June 23, 2023: Effective Date: Interagency Guidance on Third-Party Relationships: Risk Management

- July 21, 2023: Effective Date: Supervisory Guidance on Multiple Re-Presentment NSF Fees

- May 12, 2023: Effective Date: Fair Housing Rule, Consumer Protection in Sales of Insurance Rule; Technical Correction

- February 17, 2023: Effective Date: Debit Card Interchange Fees and Routing

- April 28, 2023: Effective Date: Enterprise Duty To Serve Underserved Markets-Colonia Census Tract Amendments

- June 2, 2023: Effective Date: Economic Growth Regulatory Relief and Consumer Protection Act: Implementation of National Standards for the Physical Inspection of Real Estate (NSPIRE)

- July 21, 2023: Effective Date: Policy Statement on Prudent Commercial Real Estate Loan Accommodations and Workouts

- August 11, 2023: Effective Date: Money Market Fund Reforms; Form PF Reporting Requirements for Large Liquidity Fund Advisers; Technical Amendments to Form N-CSR and Form N-1A

- September 8, 2023: Effective Date: Loan Purchase Activities: Legal Lending Limit Guidance

- September 8, 2023: Effective Date: Small Business Investment Company Investment Diversification and Growth

- June 23, 2023: Effective Date: Small Business Lending Under the Equal Credit Opportunity Act (Regulation B)

- September 8, 2023: Effective Date: FDIC Updates Equal Housing Lender Posters

- October 13, 2023: Effective Date: Adverse action notification requirements and the proper use of the CFPB’s sample forms provided in Regulation B

- November 10, 2023: Effective Date: Joint Statement on Fair Lending and Credit Opportunities for Noncitizen Borrowers Under the Equal Credit Opportunity Act

- September 8, 2023: Effective Date: Additional Guidance on Low-Income Communities Bonus Credit Program

- November 17, 2023: Effective Date: Telephone Consumer Protection Act: Revised Interagency Examination Procedures and Rescissions

- November 17, 2023: Effective Date: Commercial Lending: Venture Loans to Companies in an Early, Expansion, or Late Stage of Corporate Development

- November 17, 2023: Effective Date: Indorsement and Payment of Checks Drawn on the United States Treasury

- December 29, 2023: Effective Date: Retail Lending: Risk Management of ‘Buy Now, Pay Later’ Lending

- January 5, 2024: Effective Date: Advisory: Managing Commercial Real Estate Concentrations in a Challenging Economic Environment

- December 15, 2023: Effective Date: Federal Reserve Bank Capital Stock

- October 13, 2023: Effective Date: Truth in Lending (Regulation Z) Annual Threshold Adjustments (Credit Cards, HOEPA, and Qualified Mortgages)

- October 27, 2023: Effective Date: Regulatory Capital Rules: Risk-Based Capital Requirements for Depository Institution Holding Companies Significantly Engaged in Insurance Activities

- November 17, 2023: Effective Date: Use of FinCEN Identifiers for Reporting Beneficial Ownership Information of Entities

- December 15, 2023: Effective Date: Beneficial Ownership Information Reporting Deadline Extension for Reporting Companies Created or Registered in 2024

- December 15, 2023: Effective Date: Truth in Lending (Regulation Z)

- December 15, 2023: Effective Date: Consumer Leasing (Regulation M)

- December 15, 2023: Effective Date: Appraisals for Higher-Priced Mortgage Loans Exemption Threshold

- January 5, 2024: Effective Date: Home Mortgage Disclosure (Regulation C) Adjustment to Asset-Size Exemption Threshold

- January 5, 2024: Effective Date: Community Reinvestment Act Regulations Asset-Size Thresholds

- January 12, 2024: Effective Date: Community Reinvestment Act: Revision of Small and Intermediate Small Bank and Savings Association Asset Thresholds

- February 2, 2024: Effective Date: Notice of Annual Adjustment of the Cap on Average Total Assets That Defines Community Financial Institutions

- February 2, 2024: Effective Date: Notification of Inflation Adjustments for Civil Money Penalties

- February 2, 2024: Effective Date: Rules of Practice for Hearings

- February 2, 2024: Effective Date: Notice of Inflation Adjustments for Civil Money Penalties

- February 2, 2024: Effective Date: Securities Operations: Shortening the Standard Settlement Cycle

- February 2, 2024: Effective Date: Fair Credit Reporting; File Disclosure

- February 2, 2024: Effective Date: Fair Credit Reporting; Background Screening

- February 2, 2024: Effective Date: Financial Crimes Enforcement Network; Inflation Adjustment of Civil Monetary Penalties

- January 5, 2024: Effective Date: Beneficial Ownership Information Access and Safeguards

- April 12, 2024: Effective Date: FinCEN Publishes an Administrative Ruling Regarding Customer Identification Program and Customer Due Diligence Requirements for Designated Beneficiaries of Individual Retirement Accounts

- April 12, 2024: Effective Date: CFPB Circular 2024-02 Deceptive marketing practices about the speed or cost of sending a remittance transfer

- March 24, 2022: Effective Date: FDIC Final Rule Regarding Deposit Insurance Simplification

- November 10, 2023: Effective Date: Community Reinvestment Act

- December 15, 2023: Effective Date: Enterprise Regulatory Capital Framework-Commingled Securities, Multifamily Government Subsidy, Derivatives, and Other Enhancements

- December 15, 2023: Effective Date: Special Assessment Pursuant to Systemic Risk Determination

- January 5, 2024: Effective Date: FDIC Finalizes Rule to Modernize Official Signs and Advertising Statement Requirements for Insured Depository Institutions

- January 12, 2024: Effective Date: Rules of Practice and Procedure

- April 12, 2024: Effective Date: Community Reinvestment Act; Supplemental Rule

- May 24, 2024: Effective Date: HUD Issues Fair Housing Act Guidance on Applications of Artificial Intelligence

- May 24, 2024: Effective Date: Third-Party Risk Management A Guide for Community Banks

- April 26, 2024: Effective Date: Telemarketing Sales Rule

- May 3, 2024: Effective Date: Floodplain Management and Protection of Wetlands; Minimum Property Standards for Flood Hazard Exposure; Building to the Federal Flood Risk Management Standard

- July 12, 2024: Mortgagee Letter: Significant Cybersecurity Incident (Cyber Incident) Reporting Requirements

- July 12, 2024: Agency Information Collection Activities; Submission for OMB Review; Comment Request

- May 3, 2024: Effective Date: Defining and Delimiting the Exemptions for Executive, Administrative, Professional, Outside Sales, and Computer Employees

- July 12, 2024: Effective Date: Required Rulemaking on Personal Financial Data Rights; Industry Standard-Setting

- July 12, 2024: Effective Date: Small Business Lending Under the Equal Credit Opportunity Act (Regulation B); Extension of Compliance Dates

- January 5, 2024: Effective Date: Combating Auto Retail Scams Trade Regulation Rule

- July 12, 2024: Effective Date: Truth in Lending (Regulation Z); Use of Digital User Accounts To Access Buy Now, Pay Later Loans

- July 26, 2024: Effective Date: 7(a) Working Capital Pilot Program

- May 24, 2024: Effective Date: Reporting, Procedures and Penalties Regulations

- July 12, 2024: Effective Date: Registry of Nonbank Covered Persons Subject to Certain Agency and Court Orders

- September 3, 2024: Effective Date: Fair Hiring in Banking Act

- November 1, 2024: Effective Date: OCC Bulletin 2024-29 Commercial Lending: Refinance Risk

- November 1, 2024: Effective Date: Update to the Public Utility Exemption Under the Beneficial Ownership Information Reporting Rule

- March 21, 2025: Update to the Public Utility Exemption Under the Beneficial Ownership Information Reporting Rule Effective Date: Negative Option Rule

- March 21, 2025: Federal Reserve Bank Capital Stock

- December 13, 2022: Effective Date: HUD- Acceptance of Private Flood Insurance for FHA-Insured Mortgages

- March 21, 2025: National Flood Insurance Program Installment Payment Plan

- November 1, 2024: Effective Date: Consumer Leasing (Regulation M)

- November 1, 2024: Effective Date: Truth in Lending (Regulation Z)

- November 1, 2024: Effective Date: Appraisals for Higher-Priced Mortgage Loans Exemption Threshold

- March 21, 2025: OCC Guidelines Establishing Standards for Recovery Planning by Certain Large Insured National Banks, Insured Federal Savings Associations, and Insured Federal Branches

- March 21, 2025: Truth in Lending Act (Regulation Z) Adjustment to Asset-Size Exemption Threshold

- March 21, 2025: Home Mortgage Disclosure (Regulation C) Adjustment to Asset-Size Exemption Threshold

- March 21, 2025: Community Reinvestment Act Regulations Asset-Size Thresholds

- March 21, 2025: Debt Collection Practices (Regulation F); Deceptive and Unfair Collection of Medical Debt

- March 21, 2025: Defining Larger Participants of a Market for General-Use Digital Consumer Payment Applications

- March 21, 2025: Telemarketing Sales Rule

- March 21, 2025: Effective Date: Negative Option Rule

- August 15, 2025: Effective Date: Fees for Instantaneously Declined Transactions; Withdrawal of Proposed Rule

- March 21, 2025: Civil Penalty Inflation Adjustments

- March 21, 2025: Notice of Inflation Adjustments for Civil Money Penalties

- August 15, 2025: Effective Date: Truth in Lending (Regulation Z); Consumer Credit Offered to Borrowers in Advance of Expected Receipt of Compensation for Work

- August 15, 2025: Effective Date: Affirmatively Furthering Fair Housing; Withdrawal

- August 15, 2025: Effective Date: Reducing Barriers to HUD-Assisted Housing; Withdrawal

- August 15, 2025: Effective Date: Rules of Practice and Procedure; Civil Money Penalty Inflation Adjustment

- March 21, 2025: Required Rulemaking on Personal Financial Data Rights

- March 21, 2025: Financial Crimes Enforcement Network; Inflation Adjustment of Civil Monetary Penalties

- August 15, 2025: Effective Date: Financial Crimes Enforcement Network; Inflation Adjustment of Civil Monetary Penalties

- August 15, 2025: Effective Date: Adjustments to Civil Penalty Amounts

- August 15, 2025: Effective Date: Pausing Foreign Corrupt Practices Act Enforcement To Further American Economic and National Security

- August 15, 2025: Effective Date: Reporting, Procedures and Penalties

- April 4, 2025: Unsafe and Unsound Banking Practices: Brokered Deposits Restrictions; Guidelines Establishing Standards for Corporate Governance and Risk Management for Covered Institutions With Total Consolidated Assets of $10 Billion or More; Regulations Implementing the Change in Bank Control Act; Withdrawal

- April 4, 2025: Rescinding Multiple Appraisal Policy Related Mortgagee Letters

- April 4, 2025: Bank Supervision: Removing References to Reputation Risk

- August 15, 2025: Effective Date: Beneficial Ownership Information Reporting Requirement Revision and Deadline Extension

- August 15, 2025: Effective Date: Affirmatively Furthering Fair Housing Revisions

- March 21, 2025: Request for Information Regarding the Collection, Use, and Monetization of Consumer Payment and Other Personal Financial Data

- March 21, 2025: Request for Information Regarding the Collection, Use, and Monetization of Consumer Payment and Other Personal Financial Data

- April 4, 2025: Issuance of a Geographic Targeting Order Imposing Additional Recordkeeping and Reporting Requirements on Certain Money Services Businesses Along the Southwest Border

- August 15, 2025: Effective Date: Issuance of a Geographic Targeting Order Imposing Additional Recordkeeping and Reporting Requirements on Certain Money Services Businesses Along the Southwest Border

- August 15, 2025: Effective Date: Temporary Exceptions to FIRREA Appraisal Requirements in Los Angeles County as Affected by California Wildfires and Straight-Line Winds

- August 15, 2025: Effective Date: Restoring Equality of Opportunity and Meritocracy

- August 15, 2025: Effective Date: Interpretive Rules, Policy Statements, and Advisory Opinions; Withdrawal

- August 15, 2025: Effective Date: Protecting Americans From Harmful Data Broker Practices (Regulation V); Withdrawal of Proposed Rule

- August 15, 2025: Effective Date: Prohibited Terms and Conditions in Agreements for Consumer Financial Products or Services (Regulation AA); Withdrawal of Proposed Rule

- August 15, 2025: Effective Date: Electronic Fund Transfers Through Accounts Established Primarily for Personal, Family, or Household Purposes Using Emerging Payment Mechanisms; Withdrawal

- August 15, 2025: Effective Date: Authority of States To Enforce the Consumer Financial Protection Act of 2010; Rescission

- August 15, 2025: Effective Date: Inflation Adjustment of Civil Monetary Penalties

- August 15, 2025: Effective Date: Procedure Relating to Rulemaking; Rescission

- August 15, 2025: Effective Date: Children’s Online Privacy Protection Rule

- May 24, 2024: Effective Date: Availability of Funds and Collection of Checks

- August 15, 2025: Effective Date: International Criminal Court-Related Sanctions Regulations

- August 15, 2025: Effective Date: FCC Removes One-to-One Consent Rule Nullified by Court Decision

- August 15, 2025: Effective Date: Adjustment of Civil Monetary Penalty Amounts for 2025

- August 15, 2025: Effective Date: Parent Companies of Industrial Banks and Industrial Loan Companies; Withdrawal of Proposed Rule

- August 15, 2025: Effective Date: Rescission of State Official Notification Rules; Withdrawal

- August 15, 2025: Effective Date: Statement of Policy on Bank Merger Transactions

- August 15, 2025: Effective Date: Imposition of Special Measures Prohibiting Certain Transmittals of Funds Involving CIBanco S.A., Institution de Banca Multiple, Intercam Banco S.A., Institución de Banca Multiple, and Vector Casa de Bolsa, S.A. de C.V.; Extension of Effective Date

- August 15, 2025: Effective Date: Manufactured Home Construction and Safety Standards; Postponing Effective Date

- August 25, 2025: Modernizing Payments To and From America’s Bank Account

- March 21, 2025: Overdraft Lending: Very Large Financial Institutions

- June 10, 2025: Effective Date: Quality Control Standards for Automated Valuation Models

- January 28, 2026: Effective Date: Regulation D: Reserve Requirements of Depository Institutions

- January 28, 2026: Effective Date: Regulation A: Extensions of Credit by Federal Reserve Banks

- January 28, 2026: Effective Date: Imposition of Special Measures Prohibiting Certain Transmittals of Funds Involving CIBanco S.A., Institución de Banca Multiple, Intercam Banco S.A., Institución de Banca Multiple, and Vector Casa de Bolsa, S.A. de C.V.; Extension of Effective Date

- January 28, 2026: Effective Date: Procedures for Supervisory Designation Proceedings

- January 28, 2026: Effective Date: Catch-Up Contributions

- January 28, 2026: Effective Date: Truth in Lending Act (Regulation Z) Adjustment to Asset-Size Exemption Threshold- requirement to establish an escrow account for HPML

- January 24, 2026: Effective Date: Home Mortgage Disclosure (Regulation C) Adjustment to Asset-Size Exemption Threshold

- February 22, 2026: Effective Date: Revision of the Negative Option Rule, Withdrawal of the CARS Rule, Removal of the Non-Compete Rule To Conform These Rules to Federal Court Decisions

- May 24, 2024: Effective Date: Fair Lending, Fair Housing, and Equitable Housing Finance Plans

- March 21, 2025: FDIC Official Signs and Advertising Requirements, False Advertising, Misrepresentation of Insured Status, and Misuse of the FDIC’s Name or Logo

- February 22, 2026: Effective Date: Repeal of Fair Lending, Fair Housing, and Equitable Housing Finance Plans

- March 17, 2026: Effective Date: National Bank Chartering

- March 17, 2026: Effective Date: Rescission of 12 CFR 27, ‘Fair Housing Home Loan Data System’

- March 17, 2026: Effective Date: Community Bank Licensing Amendments: Final Rule

- April 6, 2026: Effective Date: Retirement Security Rule: Definition of an Investment Advice Fiduciary: Notice of Court Vacatur

- April 21, 2026: Effective Date: Prohibition on the Use of Reputation Risk by Regulators

- May 28, 2026: Effective Date: Real Estate Lending Escrow Accounts

- June 1, 2026: Effective Date: Preemption Determination: State Interest-on-Escrow Laws

- May 14, 2026: Effective Date: National Bank Non-Interest Charges and Fees

- May 18, 2026: Effective Date: Section 1071 Small Business Lending Final Rule

- May 14, 2026: Effective Date: Regulatory Capital Rule: Community Bank Leverage Ratio Framework

- May 13, 2026: Effective Date: Fiscal Service, Eliminating Unnecessary Regulations

- May 13, 2026: Effective Date: Equal Credit Opportunity Act (Regulation B) Final Rule

- June 24, 2026: Effective Date: Joint Rule Establishing Data Standards under the Financial Data Transparency Act of 2022

- February 4, 2026: Effective Date: FDIC Official Signs, Advertisement of Membership, False Advertising, Misrepresentation of Insured Status, and Misuse of the FDIC’s Name or Logo

- January 29, 2026: Effective Date: Delaying the Effective Date of the Anti-Money Laundering/Countering the Financing of Terrorism Program and Suspicious Activity Report Filing Requirements for Registered Investment Advisers and Exempt Reporting Advisers